Finance tells us that there are three types of attitudes towards risk, risk seeking, risk neutral and risk averse, but the pragmatic view would include a fourth, risk naïve. That is, in reality there are times when we are not fully cognizant of the risks involved and are unaware (due to ignorance or self-denial), underestimate or overestimate the risks. My bet is that most of us fall into this last category. That is why our investment regulatory framework recognizes two types of investors, wealthy, sophisticated and accredited investors, and everyone else.

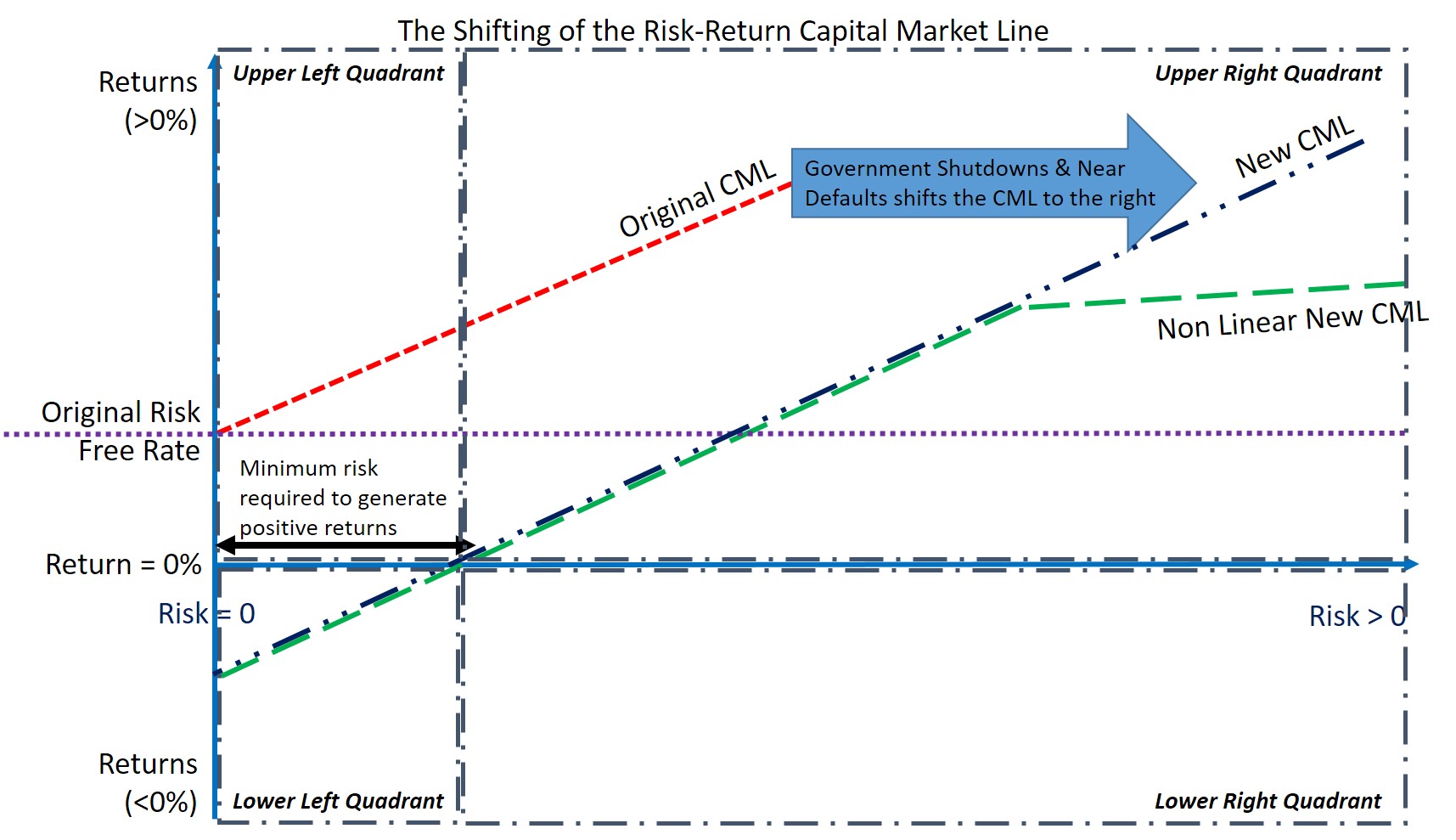

The Capital Market Line (CML) is a method of estimating risk-return. Risk is measured by volatility or the standard deviation of the returns. With existing theory one cannot be at a point above this line or exceed the returns for a given risk.

The series of government shutdowns and near defaults shows that US bonds are not risk free. That means that the CML has shifted to the right (see picture below, from red-dashed line to purple-double-dot-dashed line). That negative bond returns are feasible as happened recently in Europe.

As shown in the Lower Left Quadrant, there is a minimum amount of risk that has to be managed before one can attain positive returns. This is good news, as it shows that our government and civil service are actively managing all forms of risks to maintain a viable and functioning nation.

However, a negative GDP growth would put us in the Lower Left Quadrant, and indicates that we have not taken sufficient economic risk measures to mitigate this. That is, our legislature was not proactive to thwart unbridled greed in our banking and financial services sectors, to prevent the unwarranted Wall Street Crash of 2008 and the Great Recession.

The bad news is that:

(1) Our legislature is at times risk naïve. Imagine shutting down our government because you cannot get your way. Once the veil is torn it cannot be untorn. The American CML has shifted to the right and we cannot take that back.

Unfortunately, I do not believe that our legislatures understand the seriousness of the damage their actions have wrought on this country of ours. I pray that our legislature understand that the exercise of power in the negative is an affirmation of the lack of authority. Therefore, we need to find other alternatives to resolving conflicts in our legislatures.

The variation in the leadership of our state legislatures is also large. For example, with the Wall Street Crash of 2008 and the resulting Great Depression, California State Legislature cleaned up its banking laws to protect its citizens, while the Colorado State Legislature gold plated its Capitol Hill dome. Having lived 16 years in Colorado, I no longer believe that the Colorado State Legislature will do anything real to protect its citizens. Like water buffaloes, they have the strength to do something, but stand around and watch life go by. What a legacy to leave behind.

(2) In practice there is no such thing as risk-free. Even cash is not risk-free as the currency can devalue/revalue and inflation/deflation can alter its value. That is, we don't know the future value of anything.

From a private sector perspective, this shifted CML shows us that if there isn't sufficient capital at risk, a company cannot hope to generate positive returns. Given that all other factors are correctly implemented or addressed, insufficient capitalization is the main reason why startups fail, and why companies fail in a downturn.

For my 2 volume, 550 page master of finance thesis with the University College Dublin, I showed that the CML is not a straight line but has a substantially reduced slope as risk increases (see green-long-dashed line in the Upper Right Quadrant). That is, returns do not increase linearly with risk. At some point diminishing returns kick in. Therefore, it is prudent to manage the amount of risk one takes on, as risk-return is non-linear.

As a nation we sometimes have to take on very high-risk-ventures whose risk-returns are not acceptable to the private sector. NASA's Apollo program is a very good example. The tax payer, having funded much of this design, manufacturing and communications research now enable private entrepreneurs such as Elon Musk of SpaceX, Jeff Bezos of Blue Origin, Boeing, Lockheed, Northrop Grumman and Raytheon to build space systems and launch vehicles that are in line with private sector profitability targets.

So we need the public sector risking capital, to deliver opportunities to facilitate the profit driven capitalism, not the other way around (for example, the prosperity gospel is only taught in wealthy nations). The two, public and private sectors, go hand in hand, and it is to our shortsightedness to claim one is preferred over the other.

The reverse is true. If we don't collect enough taxes to fund risk taking, we will slip back into the negative. At the basic public sector risk taking, we employ individual civil servants to make decisions on our behalf with our tax-payer funds, to allocate these funds in good faith to deserving requirements. They overcome the risk of incorrect allocation, undeserving requirements, waste, and at times risk their own lives.

Lets face up to the fact that a grid locked legislature is unable to govern. Like they say if we don't plan our lives, others will plan for us. Therefore, others will govern on behalf of our legislature. Not good. Can we do better?

Let's not be risk naïve. Not in this most intellectually sophisticated nation on this planet. It does not behoove us to claim that we live in this greatest of nations, and then apply the three monkey stance, see no evil, hear no evil, speak no evil, or worse its opposite.