Oil prices are plunging below $50 per barrel, and the European Central Bank is about to announce whether it will begin its own Quantitative Easing program, similar to the Fed's purchase of government securities, but designed to pump more money into Europe's lagging economies. So economists are wondering whether this will have a net plus effect on growth, since the oil industry will lose profits and the EU economy is slipping back into recession.

A Saudi oil Prince sazys oil prices will stay down for a long period--years, of necessary to support their market share.

"If supply stays where it is, and demand remains weak, you better believe [the price of oil] is gonna go down more. But if some supply is taken off the market, and there's some growth in demand, prices may go up. But I'm sure we're never going to see $100 anymore,"

said Prince Alwaleed bin Talal, the billionaire Saudi businessman, in an interview with Maria Bartiromo of Fox Business News published in USA Today.

The initial result seems to be that U.S. consumer confidence is soaring as gas prices have fallen more than $1 per gallon in a year, even below $2 per gallon in many regions. But other prices are falling as well, which is worrying economists, who see it as a sign of weakening demand elsewhere. Weak demand may be elsewhere in the world, such as Europe that is slipping perilously close to recession, but it affects the U.S. economy as well.

Graph: TradingEconomics.com

Such weakness is difficult to reverse as the Japan's two decade example of outright deflation proved. It knocked them down from second to fourth largest world economy.

Europe is having the same problem, mainly due to its austerity policies that have cut back government spending, and so demand for its goods and services. Switzerland just rang the alarm bells when it very suddenly removed its 1.2 euros to Swiss Franc exchange rate cap, thus causing the SF value to skyrocket. Why did it take the cap off? There is lots of conjecture. The Swiss had been protecting their currency exchange value from rising too rapidly by buying euros, in order to protect their export industry.

But allowing the Swiss Franc to rise as much as 20 percent against the euro also raised the danger of a deflationary spiral such as happened in Japan. Why? A more expensive SF will counteract the upcoming QE purchases of the European Central Bank that are designed to put more euros into circulation in order to ease credit conditions.

.

Nobelist Paul Krugman said in a recent blog,

"By throwing in the towel on the peg to the euro, the SNB (Swiss National Bank) immediately convinced markets that its previous apparent commitment to do whatever it takes to avoid deflation is null and void. And this expectations effect trumped the concrete, immediate policy of drastically negative interest rates on reserves. It will continue to feed the deflationary trap Europe is falling into."

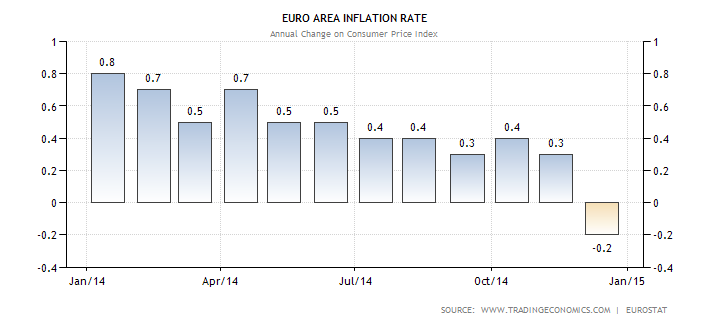

European deflation is happening in a big way. Eurozone annual inflation rate was recorded at -0.2 percent in December, matching preliminary estimates. It is the first fall in consumer prices since September of 2009, due to a drop in energy costs.

Graph: Trading Economics

In December 2014, negative annual rates were observed in sixteen Member States. The lowest annual rates were registered in Greece (-2.5 percent), Bulgaria (-2.0 percent), Spain (-1.1 percent) and Cyprus (-1.0 percent). The highest annual rates were recorded in Romania (1.0 percent), Austria (0.8 percent) and Finland (0.6 percent). Compared with November 2014, annual inflation fell in twenty-six Member States, remained stable in Sweden and rose in Estonia.

The U.S. inflation rate is still 1.3 percent, but this month's Consumer Price Index for retail prices was unchanged, which is hovering very close to deflation. Oil prices are the main culprit here as well, but falling oil prices are also a sign of slowing growth in the rest of the world; which has to ultimately affect US growth.

There is a counterbalancing effect from lower energy costs, of course. Consumers have more to spend and production costs are reduced. So prices could begin to rise again as more jobs are created. But that means no more austerity that has damaged growth in the U.S. as well, and congressional opposition to spending measures that will create more jobs. Who is willing to bet that will happen?

Paul Krugman has the last word in his latest blog.

"So the (EU) market is saying both that there are very few good investment opportunities out there -- few enough that paying the German government to protect the real value of your wealth is a good move -- and that inflation over the next five years will be around 0.4 percent, not the target of 2 percent."

So look out below for more falling prices and slowing growth, if Draghi and the ECB can't stimulate some EU growth with its upcoming QE purchases of sovereign debt.

Harlan Green © 2015