Protestor During June 2015 Greek Referendum

Protestor During June 2015 Greek Referendum

The Greek financial crisis is on the verge of entering its sixth year. The European Union has struggled to find a solution that would put Greece on a path towards fiscal solvency at a price that Greeks and the Greek government would find acceptable. Despite countless ministerial meetings, two separate Economic Adjustment Programs, Greek promises of reform, and a succession of short-term financial accommodations, Europe is no closer to solving the "Greek crisis" than it was in 2009 when the crisis started.

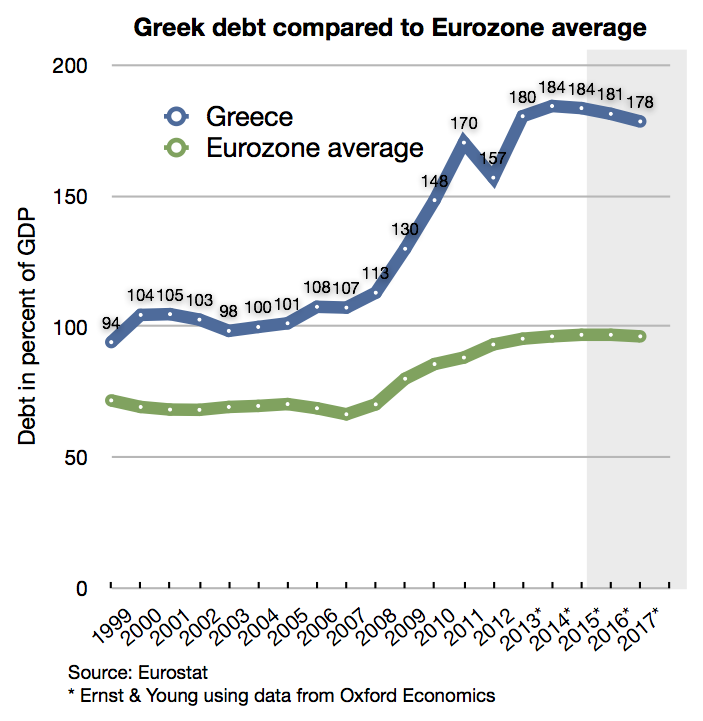

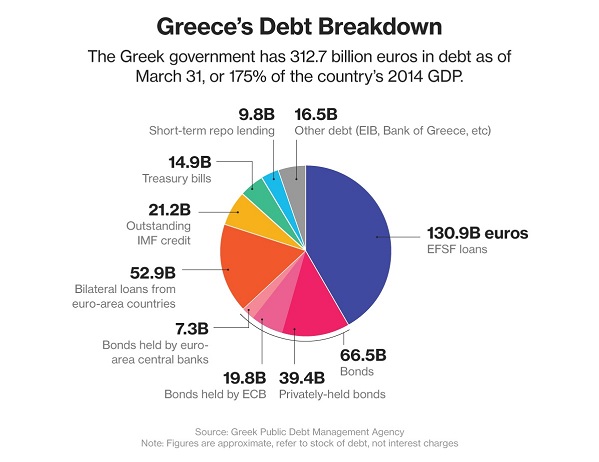

The reality is that Greece is bankrupt. With a total debt of 323 billion Euros ($352.7 billion USD), Greece's debts are now over 175% of GDP. While the sale of state owned assets would make a significant dent in the overall level of indebtedness, such sales alone are insufficient to significantly reduce Greece's debt. Improving collections of Greece's notoriously "leaky" tax system would improve government revenues, but these too would be insufficient to restore Greece's fiscal health.

Moreover, increased taxation, whether from new taxes or from more stringent application of existing taxes, would only serve to further depress economic activity. Between 2009 and 2015, Greek GDP declined by roughly 25%. In the meantime unemployment has soared to 25% while real wages, on average, have declined by 20%. While improved government revenues might allow some pay down of Greece's debt, the resulting decline in GDP would raise the ratio of debt to GDP and make the remaining debt that much more untenable.

The solution is clear enough, write-off half of Greece's debt in return for a package of economic reforms that would bring the government's revenues and expenditures into balance and as a result restore Greece to a solid fiscal footing. Such a write-off would bring Greece's debt down to around 90% of GDP, roughly in line with, if not slightly better, than the EU average.

The problem with that solution is that no one really believes that the Greek government will carry through with such reforms in the face of the inevitable public opposition that they will generate. Indeed it's not even clear whether legally the Greek government has the authority to unilaterally change, for example, the generous terms of Greece's public pension system.

Moreover, writing-off Greece's government debt is politically untenable, especially in those countries that hold a majority of Greece's debt and whose citizens see a write-off as little more than rewarding Greece's profligacy. Finally, there is a legitimate concern among Europe's creditor nations, that an overly accommodative policy towards Greece will open the door for other EU members seeking a comparable debt relief.

None of this is new. A century ago Greece found itself in similar financial straits. On that occasion, its European creditors intervened and took control of the country's fiscal affairs until fiscal order was restored. Such options, however, are no longer politically acceptable or even feasible. In an age of social media, pervasive and instantaneous media coverage and widespread political mobilization, such heavy handed tactics are simply no longer workable.

In the pre-Euro days, the solution would have been simple enough: devalue the local currency, impose controls to keep inflation in check and wages in line, and leverage the improved national competitively of labor and domestic assets to accumulate sufficient foreign exchange to pay down the national debt. That's no longer an option either. You cannot devalue your currency when you are part of a multi-nation currency union. All you can do is opt out of the currency unit in favor of a new unit of national currency.

What would happen if the Greek government opted to leave the Euro and restore the Drachma as the nation's currency, the so-called "Grexit"? Such a move would not require it to leave the EU. It would still participate in EU political deliberations in Brussels. It would still be part of the European common market. There are a number of EU members who opted not to adopt the Euro, the United Kingdom being the most notable example, but are still functioning members of the European Community.

Suppose that Athens announced that it was leaving the Euro in favor of the "New Drachma". Further suppose that the official exchange rate was set at parity, one Euro gets you one New Drachma or "Drach". Of course no one in their right mind would exchange a Euro for one New Drachma. But at some exchange rate, speculators or would be investors would be willing to trade their Euros for Drachs. The initial exchange rate is off course meaningless, the issue is where the exchange rate would eventually stabilize. Regardless of what currency restrictions the Greek government imposed, a defacto, unofficial, exchange market would develop.

The most likely scenario is that initially the unofficial exchange rate would plunge to between one-third and one-half of parity before initially stabilizing at somewhere between one-half and two-thirds of parity. Assuming that the official exchange rate stayed at a one for one exchange, this would have the effect of cutting Greece's government debt by one-third to one-half or roughly to between 90% to 120% of GDP. This level of debt would be more in line with the rest of the EU.

This is only true of course if holders of Greece's Euro denominated debt agreed to accept New Drachmas at the official exchange rate in lieu of Euros. EU financial institutions might agree to accept New Drachmas. That would be one way of slowly and quietly writing off the Greek debt. If Greece's creditors insisted on being paid in Euros, then Greece's Euro denominated debt would remain the same and as a percentage of GDP would go up by a proportionate amount based on the defacto exchange rate. In other words, expressed in New Drachmas, Greece's government debt would rise to between 240% and 360% of GDP.

Where the New Drachma-Euro exchange rate goes from there is a function to what happens with the Greek economy and the government's success in keeping inflation under control. The Greek economy is heavily dependent on imports, especially food. These would continue to be priced in Euro's, so their effective costs would increase by a factor of 50% to 100%. Priced in New Drachmas, Greece's exports and domestic assets would be far more competitive, but it would take a while before this increased competitively would be reflected in new GDP growth.

Short-term, switching out of the Euro would plunge Greece into another deep depression and, most likely, a period of widespread social unrest and political turmoil that would mitigate part of the advantage of a more competitive economy. Moreover, this reset would only work if the Greek government was able to keep its expenditures inline with its income. Otherwise, the reset only serves to start a new cycle of indebtedness and sets the stage for yet another Greek financial crisis in the future. Only in this case, instead of a Euro debt crisis it will be a Drachma debt crisis that will manifest itself as Greek hyperinflation and the concomitant political and social chaos.

There are two other wrinkles to the "New Drachma" option. First, in addition to the 300+ billion Euro of government debt, there is another 230 billion Euros of private debt. These debts range from credit card balances to home mortgages to business loans. Virtually all of the consumer and commercial debt in Greece is denominated in Euros. That is after all the country's currency. It is not entirely clear how much of that debt is owed to Greek banks and how much is owed to foreign banks. The majority is probably owed to Greek banks.

Here too, creditors and debtors face a similar dilemma. If Greek debtors are forced to pay off their Euro denominated loans with depreciating New Drachmas, their effective debt burden will increase by 50% to 100% overnight. Conversely, if Greek creditors are forced to accept repayment of their Euro denominated loans in depreciated Drachs at an "official" exchange rate they will, most likely, have to write-off between one-third and one-half of their loan balances. No financial institution can withstand these kinds of write-offs. If would completely bankrupt the Greek financial system.

Solving the Greek debt crisis will require a multi-generational solution. Already EU leaders are considering extending the maturity of Greece's loans to 2050 in the hope that by then Greek GDP will have grown to a level that will make the current debt more manageable. There is a significant problem in trying to craft a multi-generational solution however; the number of Greeks is shrinking.

Currently the Greek fertility rate (the birthrate) is hovering around 1.34 births per women. That means, on average, each Greek couple is producing only 1.34 children. For every six Greeks, there will only be four replacements in the next generation. Even with an increasing life span, the number of Greeks will steadily decline. Moreover, the average age of the population will also steadily grow older and the number of Greeks of working age, the most productive portion of the labor force, will, in another generation, be roughly half of what it is today.

Moreover, the open immigration policy of the EU means that Greek citizens can simply move to another EU country and leave all of Greece's fiscal problems behind. That option is particularly attractive to the young, Greece's future, who face 50% unemployment rates and have few assets that tie them to staying in Greece.

Keeping the Greek financial system afloat, in this scenario, would require another 100 billion Euros, give or take 20 billion. This amount would be in addition to the 100 or so billion Euros that the Greek government says it needs to continue to operate. At the moment the Greek government is close to finalizing a "Third Economic Adjustment Program" with the EU that will provide it with up to 86 billion Euros in new loans in return for carrying out various fiscal and economic reforms. Some of those new loans to Athens are not, on a net basis, new debt, they are simply new loans to pay off old loans.

Syntagma Square Protests, May 15, 2011

Syntagma Square Protests, May 15, 2011

Moreover, the EU is rapidly approaching the point of "Greek Crisis Fatigue". The reality is that the political consequences of the Greek financial crisis far outweigh the economic fallout. First, how the EU deals with Greece's financial woes will inevitably be the template that will be used for dealing with the next EU debt crisis. Too lenient an approach might well tempt other EU members to opt for a "Greek solution". A "harsher" approach, although politically more popular, will likely only prolong the crisis. The real problem is that the sources of Greece's underlying economic issues, high persistent inflation, poor tax collection, uncompetitive labor markets, a bloated and inefficient government sector, and a growing lack of economic competiveness, plague most of the EU's Mediterranean tier of members to varying degrees.

Moreover, the need to provide financial aid from the EU's richer, more fiscally prudent, members has combined with a growing concern over third world immigration into the EU and a general and continued angst about the sustainability of the "European Social Model" to spark the rise of various Euro-Skeptic political parties throughout Europe. These parties will have a long-term impact on the evolution of the EU and will constrain the freedom of action of national governments in a number of EU members making it that much more difficult to formulate an EU wide consensus.

From an economic standpoint, the Greek economy and its entire government debt is only about 2% of the EU's combined 14.3+ trillion Euro GDP. Writing off 200 to 300 billion Euros of debt is no small matter, but if it were to be written off gradually over several decades its economic impact would be minor. Long-term the EU's economic future is not dependent on whether Greece is part of the European community or whether its debts are eventually paid off or brought down to more manageable levels.

At some point, perhaps soon, the EU may opt to take the "Greek Financial Crisis" off the front burner, and the front pages, and look to downplay its importance. Treating the issue as an "administrative and technical problem", one that should be dealt with by the European Central Bank and the International Monetary Fund, rather than an EU political crisis, would give the EU's leaders some cover with their electorates and possibly diminish the appeal of the Euro-Skeptic parties.

In short, the Greek financial crisis is here to stay. The pending, Third Economic Adjustment Program, will not resolve Greece's long term debt problem, it will simply put it off into the future. The EU cannot acknowledge that Greece is bankrupt or that its Greek debts are uncollectible because, at least for now, no European leader wants to take blame for losing billions of Euros of national wealth. The Greek government lacks the political will to put its financial affairs in order and can do little more than make promises that it knows it cannot deliver on. Indeed, it is not clear that even if it was willing to accept the political turmoil and social unrest that fiscal reform would require, such reforms would be legally feasible or sufficient to restore its solvency and allow it to pay off a meaningful portion of its debts.

Moreover, to forestall a complete economic meltdown, a Greek exit from the Euro would require a level of additional fiscal support from the EU that, at this time, is simply politically untenable. Greece's ability to work its way out of its fiscal problems will diminish even more over time as a falling birthrate, a shrinking population, and the inevitable migration of the young to greener pastures will make it all the more difficult to grow GDP.

For now, the EU's leaders can do little more than string together short-term measures that maintain the façade that they are working towards a long-term solution while continuing to kick the problem down the road in the hope that it eventually will become some other leader's problem.