We are already seeing the results of Obama Administration attempts to kill Fannie Mae and Freddie Mac, the Government Sponsored Entities that guarantee more than 60 percent of all mortgages originated in the U.S. housing market these days. The Mortgage Bankers Association in particular is beginning to worry that taxpayers will have to pick up the tab in the event of another housing bust, since Fannie and Freddie aren't being allowed to maintain a capital cushion.

Obama's Treasury Department has refused to allow Fannie and Freddie to maintain a capital base as their profits decline. Instead, all their profits flow into Treasury coffers due to a 2012 amendment to the government's conservatorship agreement.

"Once their capital goes to zero, there will be no cushion between the GSEs [government-sponsored enterprises] and the need for additional draws on the remaining Treasury commitment, roughly $250 billion," said Michael Fratantoni, the MBA's chief economist and senior vice president of research and industry technology, in The Hill.

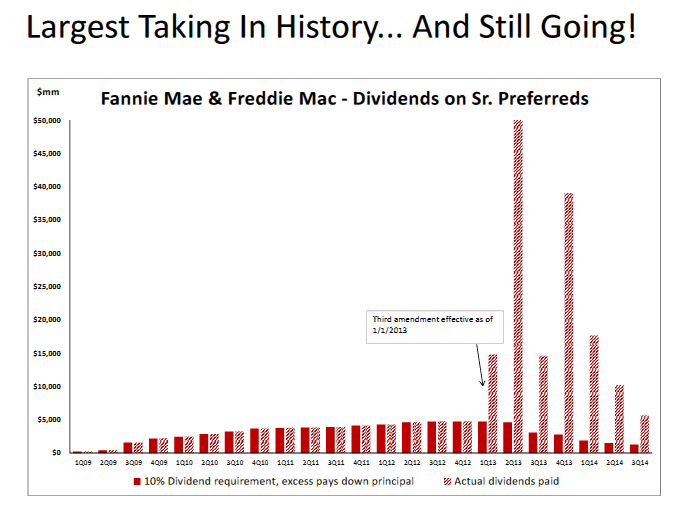

The government took over Fannie and Freddie in 2008 ostensibly to keep them from collapsing under the weight of bad mortgage debt. The two entities have drawn a total of $187.5 billion from the Treasury Department and have repaid $241 billion in dividends, though those payments don't even count toward their debt, or Treasury draw, because of Treasury's decision to commandeer all their profits.

The nominal head of Fannie and Freddie is Mel Watts, head of the Federal Housing and Finance Agency that also controls both FHA and VA mortgage agencies. And he is saying it is up to Congress to fix the problem. But Congress has done nothing, as the tug of war continues over whether the GSEs should be public-supported or solely privately funded organizations.

"I continue to hope that Congress can engage in the work of thoughtful housing finance reform before we reach a crisis of investor confidence or a crisis of any other kind," he said in a Feb. 18 speech.

In fact, the U.S. Treasury is really behind the amended conservatorship agreement that requires each firm's capital to be reduced from $1.2 billion this year to $600 million next year and then to $0 in 2018, 10 years after the financial crisis. So taxpayers will still be on the hook, unless Congress can make up its mind. But that isn't happening, and probably won't happen until after the Presidential election.

Fannie and Freddie hold a combined $5 trillion in mortgage guarantees on their books but face shrinking earnings and a zero-capital predicament -- a situation David Stevens, head of the Mortgage Bankers Association (MBA), called "unheard of." Stevens called the situation "a terrible predicament" because Fannie and Freddie "are completely critical to our housing system," according to The Hill.

Stevens said he expects that one of the GSEs will need to take a draw from the Treasury Department's credit line sometime this year -- possibly as early as the first quarter, a move likely to reverberate on Capitol Hill.

But that doesn't have to be the case, according to documents filed in lawsuits against FHFA and the Treasury Department by holders of Fannie and Freddie preferred stock rendered valueless by the amended conservatorship. For starters, analysts for the plaintiffs say, Treasury justified the conservatorship of the GSEs via accounting gimmicks since they faced no liquidity issue at the time of the crisis and recession. They note that Fannie Mae's Cash Net Income, adjusted for non-cash items was positive throughout entire crisis and recession.

Fannie Mae disclosed they held $36.3 billion cash in the bank on September 30, 2008 with a maximum exposure of roughly $6 billion per quarter. That was enough liquidity to survive over 18 months, assuming it didn't bring in another dime. But it did, leading to record profits in 2012, which is what probably triggered Treasury's takeover of their earnings.

So the last minute (2012) 'tweak' to the original conservatorship that diverted all profits into the Treasury General Fund also raised suspicions Treasury was behind the move to capture those profits for its own uses, rather than returning value to preferred stockholders. How is that fair when the GSEs weren't responsible for the bubble, or subprime loans, or the Great Recession?

We know this because some $16 billion in settlements have already been recovered from those commercial banks and Wall Street entities that submitted fraudulently underwritten mortgages misrepresenting their loan quality to Fannie and Freddie.

Why has the White House resisted calls to unseal their documents in pending lawsuits by preferred stockholders attempting to recoup losses due to the conservatorship? Antonio Weiss,, a Treasury counselor, gave their only response to Bloomberg News.

"Some have suggested the federal government could stop supporting Fannie and Freddie in the near term by allowing the companies to retain their earnings. This overlooks the high level of capital required to adequately cover the risk of the $5 trillion in assets on the GSEs' books. A recent analysis from Moody's and the Urban Institute made clear that it could take decades for Fannie and Freddie to build safe and sound levels of capital and that recap and release would ultimately drive up the cost of mortgages."

So this is the Treasury and White House response--inaction. Let's keep the taxpayer on the hook for all losses in the event of another downturn, rather than allowing the GSE's to begin to build their capital base again.

It may therefore be up to the courts to decide who is at fault in the continuing debacle--at a time of record low interest rates and a housing market just beginning to recover.

Harlan Green © 2016

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen