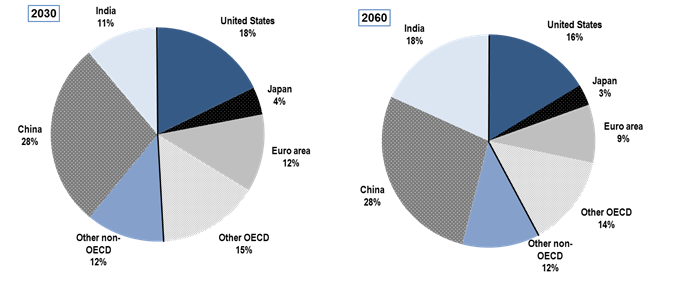

Over the past 30 years, global economic geography has radically shifted toward the East, with the center now lying just east of Mumbai. In a belated recognition of the shift in global economic power, if not yet political power, the Obama administration announced in 2013 a "pivot to East Asia," with the aims of growing security, political and economic ties with the region's countries and of "containing China." The GCC countries should undertake a similar strategic pivot of their political, economic and financial policies toward Asia and the East, with the aim of embracing China, not "containing" it. The Gulf region needs to develop its bilateral and multilateral relations with Asia and China, building on existing trade and investment relations. The policy focus should be to revive and build a "New Silk Road" that passes south of the old Silk Road. This "New Silk Road" represents the global demand and supply chains emerging from China whose tendrils are growing into Asia, Africa, the Middle East and Latin America.

The tectonic shift in global economic and financial geography undermines the inherited web of alliances, institutions and treaties forged in the aftermath of WW II. The global financial crisis that shattered the American financial empire in 2008 accelerated the Asia and eastward shift. Gulf policymakers need to awaken to this new economic reality and forge new alliances and partnerships to become an integral part of and builders of the New Silk Road.

As we enter the Chinese New Year of the Horse, China's trade with the GCC countries accounts for some 70 percent of Sino-Arab trade and 3 percent of China's global trade having grown tremendously from 1 percent in the 1990s. This trend is likely to continue given the anemic growth prospects and secular decline of Europe and US compared to EMEs. China has overtaken the US as the largest exporter to the GCC with exports growing to $60 billion a year in the last decade. Exports from GCC to China in 2012 were $101 billion. Among the GCC, Saudi Arabia was the major exporter followed up by UAE and Oman. China now sources 35 percent of its oil imports from GCC countries, in particular Saudi Arabia. Saudi Arabia is now China's largest source of crude oil imports, supplying more than one fifth of Beijing's crude imports and replacing the US as the Kingdom's top export partner. McKinsey forecasts that by 2020, total trade flows between China and the Middle East will mushroom to between $350-500 billion, with China-GCC trade accounting for the majority share.

Given their energy natural resources, the Middle East and Gulf countries are strategic trade and investment partners for an energy-hungry and deficient China. Energy has been the main driving force in the development of the China-GCC economic relationship, but the future is likely to be fundamentally different as both China and the GCC diversify their economies and Chines goods, products and services gradually displace their Western counterparts and Geely, Cherry, Great Wall, Lifan become household names and drive out GM, Chevrolet, Fiat, Opel and Peugeot. For the foreseeable future we will be dancing to a Chinese tune.

The Gulf is the natural bridge between Asia and Africa

Given its location at the mouth of the Gulf, international connectivity, growing linkages to Africa, the quality and efficiency of its infrastructure, the UAE is now the logistics hub for China: some 70 percent of Chinese exports are re-exported via the UAE to the other GCC countries, India, Iran, East and North Africa. In addition to trade flows, China-GCC investment flows have been on the rise as GCC economies remove restrictions to foreign investment and increase the diversification of their economies.

Africa is now a key recipient of Chinese FDI which is leading to a transformation of African economies and their international connectedness. The UAE with its central geographic position midway between Africa and China, its superior transport infrastructure, logistics and connectivity, has become China's gateway into Africa. Chinese trading, investment, development and contracting companies based in the UAE are transforming Africa. For the emerging African economies, the GCC and especially the UAE is the natural hub for trade with Asia and China.

Dubai, one of the most open cities in the region, is already home to over 150,000 Chinese residents; with some 3,000 Chinese companies registered in the Emirate, up from just 18 in 2005. After China and the UAE eased bilateral visa regulations in September 2009 and the UAE obtaining "approved destination status", the number of annual Chinese travelers pouring into the Gulf state mushroomed to over 300,000. They are also big-ticket spenders, as evidenced by their strong contribution to sales during the Dubai Shopping Festival period and Chinese holidays.

Four Pillars to "Pivot East"

The symbiotic energy relationship between China and the Gulf represents the past. The future should be based on more solid, less "liquid," building blocks. There are four.

One, prioritize negotiations of the China-GCC Free Trade Agreement which have been treading water since July 2004. The stakes are high: China is now the main trade partner of the GCC. The policy framework should be put in place to remove barriers to trade (including services), allow market access and investment and facilitate the multilateral rights of company establishment and joint ventures. The China-GCC FTA should also ease cooperation between State Owned and Government Related Enterprises which are dominant in both China and the GCC countries. Similarly, cooperation and joint investment between the Sovereign Wealth Funds of the two parties, which hold liquid assets in excess of $7 trillion mainly invested in Western markets and government securities, would lead to wiser investment in financing economic development in Asia/China, the Middle East, Africa and other emerging markets where the real returns are more promising.

A China-GCC FTA should build on the GCC-Singapore FTA (negotiations started in 2008 and only now coming into force!) and would be a prelude to a wider GCC-Association of South East Asian Nations (ASEAN) FTA which would complement a China FTA.

Two, the GCC banking and financial system should be integrated into the emerging "Redback Zone" where payments, capital markets and banking and financial assets and transactions will be based on the Renminbi as an international currency. Given Europe's (and the US's) economic and fiscal turmoil and tightening regulatory straitjackets, Western banks will be facing the four R's of regulation, recapitalization, restructuring and retrenchment, while continuing to bear the aftermath of the Great Recession, the fifth R. Western banks and financial institutions are divesting and will be increasingly constrained in their traditional role of financing trade and investment in our region. Chinese and Asian banks need to seize the opportunity and develop their banking and financial links in the region. The RMB should be used to finance, clear and settle trade between the Middle East, the GCC and China. It is economically inefficient to use dollars and euros to finance GCC-China trade and investment links! There is no economic or financial reason why the oil and gas exports of the GCC to China should not be denominated and payment settled in RMB. This would lower transactions costs and diminish risks.

The shift has started. The PBoC & the UAE Central Bank have taken the first step in establishing a bilateral RMB swap line which creates the liquidity and financial facilities to ease trade and investment transactions. RMB swap lines should be extended to the other GCC central banks. Given the proportionality between the volume of trade and the required level of swap lines, a GCC-China Renminbi swap line would amount to about RMB 180-200bn, given that the GCC countries account for about 2.5 percent of China's total trade (somewhat larger than Singapore). Such a proposed China-GCC RMB swap agreement would strengthen the banking and financial links and help promote trade and investment flows.

More generally, as Asian -- including India -- and other countries become increasingly integrated into China's global supply chain, the RMB will be increasingly used to finance trade along the "New Silk Road." By 2015 it will become the third world currency alongside the US dollar and the Euro. For the GCC countries the RMB will be the currency and means of payment underlying the New Silk Road.

Three, establish a Renewable Energy (RE) and nanotech partnership between the GCC and Asia/China. China has emerged as the world's clean energy and clean tech powerhouse. The UAE and GCC need to develop an industrial partnership with China to jointly undertake R&D in RE, water resource management and build solar power technology and energy capacity. Given their geographic and climatic comparative advantage, the GCC can become the global solar powerhouse building on Chinese technology and knowhow. Indeed the GCC countries can become major exporters of solar power energy and technologies. This will enable a new export production sector to emerge and, more importantly, create new job opportunities. The MENA region has significant resources in solar, wind and Carbon Capture and Storage. With its climate, location, natural and financial resources, its potential extends beyond hosting IRENA HQ. Similarly, nanomaterials are largely carbon and hydrocarbon based, offering great potential for the GCC countries to use their plentiful resources to invest in nanotechnology and become producers and exporters of nanomaterials and technology.

Four, the GCC and China should establish a security framework agreement to protect their joint interests. The Gulf and the Middle East is a region of conflicts, tensions and vulnerabilities that have been exacerbated by the Arab Firestorm. These tensions reflect, among other factors, competition and conflict for the rich energy resources of a region that contains 48.4 percent of the world's oil and some 43 percent of its natural gas. As the US retrenches, "pivots east" and redeploys its military assets, China and the GCC will need to ensure that no security vacuum emerges to threaten their strategic interests and the growing New Silk Road. Over the coming decades China will grow its "soft power" but will also build its military and strategic assets as befits a super-power. Given its high dependence on the energy resources of the Gulf China will seek to insure its energy security, while the GCC will want to protect its energy reserves and associated infrastructure. The outlines of a future alliance are in the making.

Pivoting East in a New Multi-Polar World

A new multi-polar world has emerged over the past 30 years that has shattered the post-WW II paradigm and structure, and the near hegemony of the US whose economic, financial and military power is waning. Over this same period the GCC countries have grown their economies based on an energy market dominated by Europe and the US and to a lesser extent Japan. That world is no longer. The new world order requires a re-assessment of strategy and policies and a pivot to the East by the GCC countries, to be integrated into the New Silk Road. The building blocks include a free trade agreement with China and ASEAN, integration into the "Redback Zone," a partnership with China to develop renewable energy, Nano and clean technologies and eventually a supportive security agreement. There is much to look forward to in this "brave new world."