Monetary unions have a tendency to divide participating countries to losers and winners. The Eurozone is no different. The dawning recovery of the Eurozone has raised some headlines during the winter. Recent positive growth figures from the economies of Spain, Portugal and even Greece have added to the optimism of long awaited recovery of the Eurozone. However, at the same time some new countries, like Finland, are facing serious economic hurdles, poverty in the euro area is at all-time high and youth unemployment remains highly elevated. Any kind of economic recovery would thus be warmly welcomed in the Eurozone (from now on EZ).

The only problem is that a real recovery is highly unlikely. Even if the EZ as whole would regain sustained GDP per capita growth, deeply rooted productivity differences would make the recovery an uneven one. The flow of funds and production from low productivity countries to highly productive countries is likely to continue in spite of the level of recovery, which is partly reflected in the renewed grow of the Target2 imbalances. These capital flows are also extremely hard to reverse, which will lead to persistent divergence in the living standards within the EZ. Only a transfer union could even out the effects of these asymmetric shocks, but for that there is no political will.

Persistent productivity differences

Two years ago I co-authored a study where we looked into the roots of the European debt crisis (link, in Finnish). We found three main causes for the crisis:

1. Productivity differences between the US and Europe started to widen after mid 1990's2. Productivity started to diverge between countries of the Eurozone after the formation of the euro3. Because prices in the EZ converged, productivity differences lead to differences in competitiveness, which in turn lead to the debt driven boom in government expenditures in countries with low productivity.

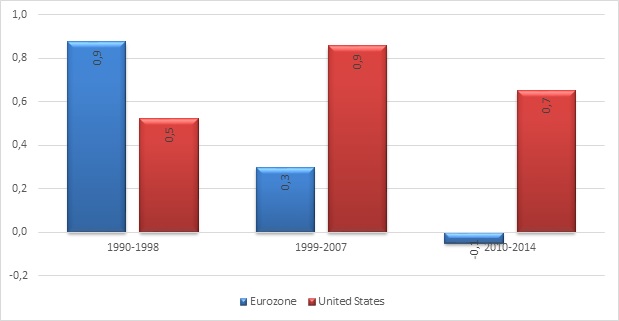

These productivity differences are clearly visible from the data. First figure below presents the growth of the total factor productivity (TFP) in the US and in the 11 original members (Greece joined in 2001) of the EZ. (Source: Conference Board, Total Economy Database)

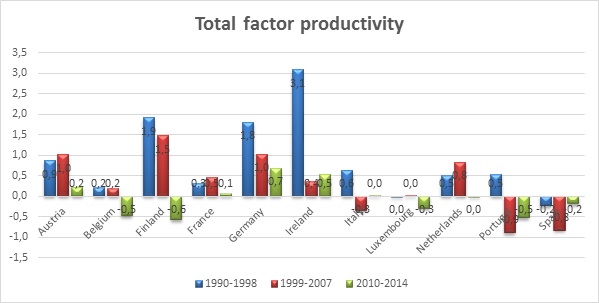

The figure shows us that, while the growth of TFP of the countries of the EZ clearly outperformed the TFP growth of the US before the creation of the EZ, during the EZ the TFP growth has been feeble. If we break the TFP growth of the Eurozone to individual countries, we see that it has slowed in every member county after they joined the zone, except in Austria and the Netherlands.

In our study, we found that the differences in TFP between countries of the EMU are likely to be explained by cultural differences, which control the adoption of new technology and differences in the resources devoted to research and development. In a recent working paper, S. Beugelsdijk, M. Klasing and P. Milionis find that agglomeration, the different knowledge-based externalities (e.g., income and education), historical path-dependence and cultural factors explain differences in productivity in Europe.

What makes these factors problematic for the EZ is that only a few of them (like investments in research and development, R&D) can be altered easily. Many factors, like path-dependence and knowledge-based externalities, tend to be deeply rooted in the culture and changing them requires both considerable effort and time. Because prices within a monetary union tend to converge, productivity differences create differences in competitiveness. What this means is that the most competitive countries, like Germany and Austria, set the conditions, i.e. the level of productivity, which countries have to meet to be able to grow in the EZ. Because productivity differences are caused by persistent factors, EZ will lead to a permanent fall in the living standards in those countries that are unable to meet the standards of productivity set by Germany.

Eurozone will continue to create losers and winnersIt took the US over 150 years, several depressions and a Civil War before it enacted fiscal federal transfers to ease the effects of asymmetric shocks. According to H. Rockoff, the dollar union would have been likely to be broken down during the Great Depression if gratuitous federal fiscal transfers and federal deposit insurance would not have been executed.

Currently, there are no signs of such political will in the EZ. Each country would need to contribute to the federal budget by the amount of 15 - 20 % of GDP (see page 41), to make the EZ an effective transfer union. Especially in the northern countries, like Finland, it is hard to imagine a situation where their citizens would be willing to transfer this amount of their income to the federal budget and to southern countries. This may, of course, eventually come to be, but it is likely to take a long time. While we are waiting, euro will continue to create income disparities, poverty and human misery among its members.

Without a transfer union, euro will bring prosperity only to its strongest (the most productive) members. Would there be a renewed recession in the EZ, productivity differences would magnify the effects of the downturn in the members with low productivity. This could create a catastrophic backlash for the political will for staying in the monetary union. Thus, although the situation in the euro area appears calm, it may easily flare up again.