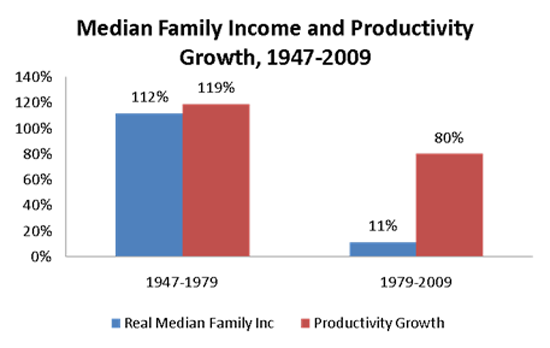

I've been working on explaining pictures like the one below, trying to understand why middle-class incomes so dramatically stopped tracking productivity growth. Productivity gains are society's main path to improved living standards, but if those gains elude the middle class, it's not a reach to say that the glue holding our society together starts to weaken.

Sources: BLS, Census Bureau

There are many reasons for this split and I'll try to get to all the ones I can think of in coming days, but here's one of my favorite, presented in a slightly complex, but hopefully intelligible way.

The diminished ability to bargain for their fair share of productivity growth is a major factor in the productivity/income split.

You may think I'm talking unions here, but I'm not. I'm talking high unemployment. (Unions matter too and I'll get back to their role.)

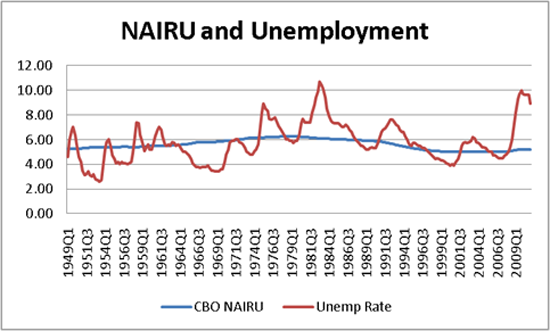

The figure below plots the unemployment rate since the 1950s against a construct called the NAIRU--it's the flat line, and it's an acronym that stands for the lowest unemployment can go without triggering runaway inflation. You don't have to buy the concept to agree with the analysis, though you should know that the NAIRU, as calculated by the Congressional Budget Office, moves around over time a bit to adjust for things like an older workforce.

Sources: BLS, CBO

Typically, unemployment will wiggle around the full employment level, below it for a while in periods of strong growth and visa-versa. When unemployment hugs the line, we're close to full employment, a very good place to be. The last time we hung out there for a while, in the latter 1990s (actually, we were below the line for a while) wages and incomes of the middle class actually tracked productivity, at least for a New York minute (and, for the record, inflation did not accelerate--but that's another story).

But here's the problem: we used to spend a lot more time below the line and a lot less above it, and in those days, middle-class incomes tracked productivity.

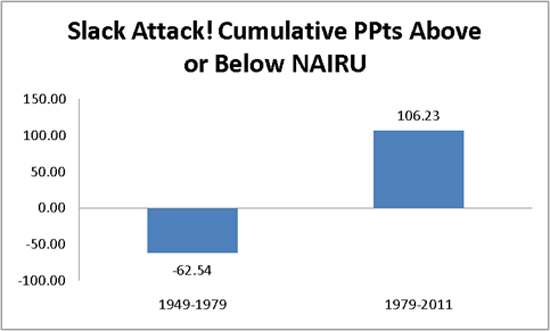

Source: Previous figure

This figure simply sums up the percentage points above or below the line over the periods when middle-class income rose along with growth and when they did not. Over the period when growth and incomes were linked, we were 60 percentage points below the line, meaning labor markets were generally very tight. When growth and income became delinked, we spent over 100 points above the line, signaling weak job markets, high unemployment, jobless recoveries, and therefore much diminished bargaining power for middle- and lower-income workers.

There's a lot more to this story and I'll try to stick with it. But the moral of the story, as the latter 1990s showed (that NY minute I referred to above), in today's global, low-union world, the working man and woman really have no better friend than full employment. It's one of the only and best ways I know to relink growth and middle-class prosperity. And we're currently nowhere near it.

This post originally appeared at Jared Bernstein's On The Economy blog.