On May 5, 2009, I testified in front of Barney Frank's Financial Services Committee that if

Congress provided a guarantee of municipal bonds, the United States of America would lose its'

AAA credit rating. Over the next year-and-a-half, I was labeled the "typical Orange County

ultra-conservative alarmist" when I spoke at dozens of investment conferences on growing risks

of munis to investors. Even as the general market price of long term munis dropped over 20% in

the fourth quarter of last year, virtually every major Wall Street investment bank continued to

reassure investors that municipal bonds were a great buy. All that hoopla ended yesterday, when Jamie Dimon, the CEO of JP Morgan Chase Bank, acknowledged at a U.S. Chamber of

Commerce event in Washington D.C., that hundreds of tax free municipal bonds issues will "not

make it" and default.

Mr. Dimon has intimate knowledge of the municipal bond market, because his firm is the third

largest underwriter and issued $47 billion of munis last year. Mr. Dimon added: "I don't think

it's going to shatter America, I just think it's a part of the credit cycle." Mr. Dimon and his bank

have obviously sold their municipal bond holdings, but perhaps the timing of the release of this

insider's perspective on a coming market crash has something to do with his bank's own needs.

Currently there are 50,000 municipal bond issuers in America and they have sold over $3 trillion in bonds to mostly individuals, mutual funds and money market funds. A good portion of tax free bond sales were to fund local government worthy projects, such as roads, schools and even city halls. But another huge portion of the money raised in the municipal bond market has gone to support politically connected contractors and other crony capitalists.

Mr. Dimon has real insider knowledge of this dark side of the muni market; since his firm

in 2009 paid $75 million in penalties and forfeited $647 million to settle SEC charges in an alleged municipal bond kick-back and derivative scam. It seems those nice people at JP Morgan Chase somehow got $3.5 billion in underwriting business after sprinkling $8 million in cash on the friends of elected sanitation officials in Alabama. If one issuer alone could cost a bank almost three quarters of a billion dollars, how much could hundreds of defaults cause the banking industry? And, what if it turns out thousands of these muni deals were tainted by pay to play? How much more could a coming market crash cost the banking industry?

Many Americans believe the current financial problems that state and local government are

going through are due to high unemployment costs and lower income taxes, but the majority of

state and local revenues come from property taxes. If U.S. property tax revenues had risen at the rate of inflation since the start of the real estate bubble in 1996, total property taxes collected this year would have been $296 billion. But collections last year totaled $476 billion, 60% or $180 billion more than inflation. Furthermore, instead of falling back by the 33% plummet in home values since 2006, property taxes rose another 27% or over $100 billion since 2006.

The reason for the rising property taxes in this dreadful property market is that local government has been wildly efficient in raising assessed values of property, but incredibly inefficient in cutting values. This has started to create a tax revolt that is growing very rapidly as homeowners are appealing or litigating to drive their property tax bills down.

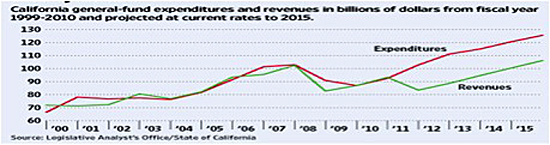

Below is a chart of the State of California projected tax revenues versus budget expenditures.

The fastest growing budget cost is snowballing interest and principal payments for municipal

bonds. Ten years ago these bond payments were only 3% of the budget, but in two years they

will reach 10% of the budget. The State revenue projections shockingly assume property taxes

collections do not decline, but a 30% decline in assessed values would cost the state $20 billion.

Jamie Dimon is one of the smartest bankers in the world and he fully understands his bank and

the rest of the banks are facing a muni bond financial meltdown. The banking industry recently used their money and power to get Congress to stick taxpayers with the $3 trillion bailout of the banks' busted mortgage loans. The bail-out was so successful for Mr. Dimon, that last year he pocketed a $17 million bonus.

I believe Mr. Dimon's new-found honesty about the risks of municipal bond defaults is part of a

strategy to convince Congress to once again saddle taxpayers with a bailout of state and local

government. From Mr. Dimon's perspective, JP Morgan Chase Bank should be about bonuses and taxpayers should be about bailouts.