Health insurance coverage of contraceptives like hormonal implants, patches and vaginal rings remains inconsistent for American women, even though the Affordable Care Act requires no-cost access to birth control, according to a report published Thursday.

Women who seek contraceptives other than the pill may find that their insurers charge copayments, require prior approval from a doctor or simply don’t cover their preferred method, the Henry J. Kaiser Family Foundation and the Lewin Group discovered in a survey of 20 health insurance companies in five states.

The Obamacare birth control mandate, which promises access to FDA-approved contraceptives at no charge from the pharmacy or doctor’s office, is imperfect in practice, the survey shows. Although access to no-cost contraception has significantly increased since this part of the Affordable Care Act took effect in 2012, health insurance companies still restrict access to some forms of birth control. The survey also found that it’s difficult for many women to understand what their health plans cover, and to compare one plan to another when choosing what insurance to buy.

“For many women, the ACA’s contraceptive coverage provision has reduced their health care out-of-pocket costs and given them the opportunity to use more effective but more costly methods of contraception that had been unaffordable to them in the past,” the report says. “For some, however, their choice of plan may still result in limitations of their contraceptive options."

Insurance companies are interpreting the law and guidance from the Department of Health and Human Services in a number of different ways, the researchers conclude.

Although the Affordable Care Act requires health insurance companies to offer no-cost birth control, it doesn’t require them to cover every form of contraception, and it permits them to levy copayments and other charges to certain types, as they do with other medications and procedures. For example, a health insurance plan might cover generic oral contraceptives at no charge, but it might not do the same for all brand-name birth control drugs, or it might require a patient to obtain her pills via mail order.

A small and shrinking percentage of women remain enrolled in health plans still “grandfathered” from Obamacare rules, and some employers are allowed to deny contraception coverage for religious reasons.

The Kaiser/Lewin survey examined health insurance benefits for seven categories of female birth control, but it didn’t include oral contraceptives, the most popular form of pregnancy prevention in the U.S. among women who use birth control. The Kaiser Family Foundation and the Lewin Group studied insurance coverage of emergency contraception; hormonal implants; hormonal injections; hormonal patches; the intrauterine device, or IUD; vaginal rings; and sterilization. The unnamed insurers were located in California, Georgia, Michigan, New Jersey and Texas.

Note: "RMM" stands for "reasonable medication management" tools, which insurers use to control costs.

Source: Henry J. Kaiser Family Foundation

The NuvaRing, a brand-name vaginal ring that transmits hormones internally and has no generic version, was found to be the least likely method to be covered by insurance at no charge. Five of the insurers required cost-sharing and one didn’t cover NuvaRing at all, the survey found.

Insurers that limit access to methods like implants, injections, patches and rings justified their policies by noting that these forms of contraception deliver the same hormones as pills that are included in their benefits, regardless of the preferences of women and their doctors, according to the survey.

Navigating the various policies for coverage of those different forms of contraception isn’t easy for many women, the report notes. In fact, it wasn't even easy for the people conducting the survey.

“One of the cross-cutting findings of this analysis was how difficult it is to ascertain the limits on contraceptive coverage used by different carriers. The contraceptive coverage policies used by health insurance carriers were not easily accessible,” the report says. “This information is even more opaque in many of the plan materials available to policyholders.”

Furthermore, the survey revealed that health insurance companies don’t appear to have required systems in place for women to appeal and gain access to forms of contraception recommended by their physicians. The Affordable Care Act calls for insurers to provide a special system for contraception appeals that's separate from the one used for other cases.

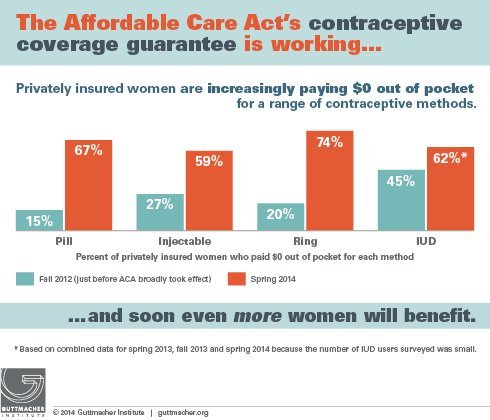

Source: The Guttmacher Institute

Women who believe they have inappropriately been denied coverage for contraception can seek help. For those who get their insurance from an employer, a human resources professional may be able to explain the health plan's benefits and intervene with the insurer. Health insurers themselves can assist in some cases, such as when a pharmacy incorrectly charges a copayment. Additional information and guidance is available from organizations such as the National Women's Law Center and Planned Parenthood Action Fund.